BLOG

INTERESTING STUFF

THAT CAUGHT OUR EYE

Brexit Housing Market Update: Are Property Prices Too Low?

Jeremy McGivern is Managing Director of Mercury Homesearch, London’s premier search agents and sales negotiatiors for luxury properties. This month, we once again invited him to share his insight on London’s high end property market.

London Luxury Property News Roundup

- Official quarterly data published by the FCA and the Prudential Regulation Authority showed the outstanding value of all residential mortgages in mid-2018 was £1.4tn.

- Savills calculated there was £5.3tn residing in UK housing equity in 2018.

- A recent report by the UK’s biggest mortgage lender, the Halifax, said that fewer homes had been on the market in 2018 than in any year of the past decade. (BBC)

- London property still stacks up favourably, when one considers buying, selling and holding costs over 5 years. Vancouver is the most expensive city followed by Hong Kong, Singapore, Tokyo, Sydney, Berlin, Paris, New York, London, San Francisco, Dubai, Shanghai, Mumbai, Dublin, Moscow. Longer timescales are even more favourable for London as holding costs are low. (Savills)

- Work started on just 3,655 new private flats and houses in London between June and September – down from 7,153 in the previous 3 months. That is the fewest since Q3 2012 The government’s target for new properties in London is 65,000 per annum (Molior)

- On 30th September 2018. the number of newly completed but unsold properties in the capital had jumped to 2,374 units. However, only 101 of these were in Kensington & Chelsea and 119 in Westminster according to figures by Molior

- London’s population is expected to be 11.27m by 2050. It is currently 8,787,892 according to the office for National Statistics.

- US money supply in 1907 was $7 billion and in 2014 it was c. £13,291 billion (Visual Capitalist)

Are Property Prices Too Low?

I had an operation on my shoulder in November which I would normally say was a bad thing but has turned out to be a blessing in disguise.

It is saving me a fortune in TV screens as I am currently incapable of hurling even light objects with any force at the television as one politician after another lines up to say something crass about Brexit.

Now, you may be thinking, McGivern you simpleton, the answer is obvious: just turn off the TV. Which I would do but, unfortunately, I need to be vaguely aware of what our beloved leaders are saying so that I can answer our members’ questions.

As it happens, they are as bored of Brexit as the rest of us – this is true of our European as well as British and other international members. Indeed, I was recently having a conversation with one of them.

We acquired him a fantastic home with direct access to communal gardens and he wants to acquire another property in London and one in the country. I pointed out to him that he was very much in the minority and that while I agreed that now is a great time to be buying property in London, I was interested to know what his reasoning was.

He said it was very simple: “If the UK were a company you would say it was great but in need of a decent CEO and board of directors”.

But we shouldn’t get too melancholy about the state of government in the U.K. I am constantly telling our international members how incompetent many of our politicians are and every single one has responded along the lines of:

“We couldn’t agree more, but you should come and see ours!”

We do not have a monopoly on political buffoonery and compared to what many people have to suffer in less stable political jurisdictions, Brexit is but a mere ripple.

And despite all the political shenanigans, the UK has actually been doing pretty well, which rather brings to mind a couple of Warren Buffett’s thoughts on investing in companies and how management is less important than a good company:

- “If you’ve got a good enough business… you know, your idiot nephew could run it. And if you’ve got a really good business, it (management) doesn’t make any difference.”

- “When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

There are not many countries that fit into the first group but there are a whole host that exist in the second. The simple fact is that the UK is great despite and not because of its politicians.

Err, what the hell has this got to do with London property?

Don’t worry, I am getting there.

Brexit has been such a divisive issue because the fundamental question was overly simplistic. Below is the voting card we were given:

17,410,742 voted to leave the EU while over 15m voted to remain.

It is the simplicity of the question that has been the problem because people’s attitudes to Europe are far more nuanced and complex. If you asked those 17 million people what they didn’t like about the EU, how they envisaged life outside of the EU and what relationship they would like to have with our friends in Europe then you would get thousands of different answers.

So, although there may be no such thing as a stupid question, an overly simplistic question almost guarantees misleading answers/poor solutions if further questions or debate are not allowed (a second referendum would just be repeating the initial simplistic question).

The same is equally true for the simple question “are London property prices too high?” (I told you I’d get there in the end). Actually, this rarely appears as a question but is almost always a statement that people agree with and assume is fact…

But too high compared to what and too high for whom? Most people just look at past prices and because they are higher now, assume that prices are too high. For example, the market crashed after we saw record prices in 2007, yet prices are now 60%+ higher than they were then. so according to conventional wisdom, we are in dangerous territory.

Add in higher stamp duty & political uncertainty and mainstream opinion will tell you that it is evident that prices must continue to fall or at best will only creep up. So, factoring everything in it would seem wiser to rent than to buy. And as rental yields are so low investing seems nonsensical.

And they would be right if there was a finite supply of money that had stayed the same, but there isn’t and it hasn’t. The facts and reality are far more complex than the simplistic arguments normally trotted out in the press which is why conventional wisdom is invariably wrong.

Those who say prices are too high are going to be shocked at how much higher they can go.

This has been true throughout history. Prices almost always seem high when looked at in terms of historic prices, but that is a woefully simplistic way of looking at anything. For example, in 1982, the S&P 500 was at 285, so when it reached 1000 in 1995 it seemed positively mad (and would have seemed impossible in 1982). Yet look at it now.

Prices are not too high just because they are at record levels. You have to consider the underlying factors of which there are several, but the amount of money in the world is a key one.

If there is more money in the world, being generated in bigger amounts and more quickly than ever before, do you not think that land prices and therefore property prices will increase (not to mention the prices of other assets)? And remember most other “products” are getting cheaper – these cost savings invariably end up in the land price (one of the big secrets that the masses fail to grasp).

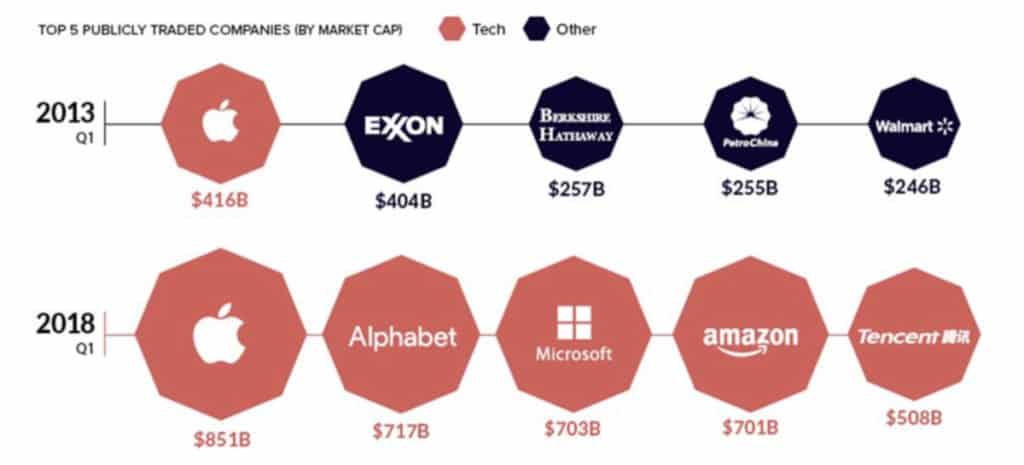

Do you think there will be more or less money in the world in 10 years’ time? History suggests that there will be considerably more and the speed of the growth in wealth globally is extraordinary. Just look at the chart below (Source: Visualcapitalist.com):

As you can see above, companies like Apple, Amazon, and Microsoft have supplanted traditional blue-chip companies and have boomed in size in just five years.

The tech invasion is leveraging connectivity, artificial intelligence and the ability to scale rapidly to create global platforms that are changing the way we live. The tech invasion has already caused radical changes in retail and now these disruptive forces have their eyes set on healthcare, finance, manufacturing and education to name but a few.

The web is virtual real estate and is allowing people to generate huge wealth as one is no longer confined by not being able to own a shop, warehouse, factory, etc. It allows people to sell information and ideas. But like the real world, popular real estate is expensive, e.g. I looked at buying the URL for Thewealthchannel.com. It’s available for c.$35k.

But while the web is a new frontier with no physical boundaries, land isn’t endless and good quality cities are actually few and far between when it comes to offering the “whole package” – New York & London top the list and will benefit from a disproportionate inflow of money accordingly.

Indeed, there are other cities and resorts that will benefit – there is a cachet to owning a property in London, New York, Val d’Isere, St. Tropez, the Bahamas, etc. which doesn’t exist to the same degree in Frankfurt, Milan, Barcelona, Madrid, Lisbon, Sydney, etc.

That’s not to say these aren’t great cities, but they do not offer the breadth of opportunity, experiences, accessibility and security as London & New York; the fact that English is the main language should not be underestimated either and nor should the education systems in both the UK & U.S.

But surely prices can’t go any higher, scream the naysayers. Look at yields they are pitiful.

Well the yield argument is hugely misleading – I know this statement will have people rolling their eyes. But look at growth shares – they increase dramatically in value despite yielding nothing.

Ahh, I hear you say, but these companies are not paying dividends because they are growing and it is more profitable to use those funds to continue the expansion and increase the share price.

Well, the same is true for property or more accurately land prices. When you buy a home or investment what you are actually buying is the land value plus the value of the property itself.

This is a vital distinction especially in London, New York, Hong Kong and a few other global mega hubs, where the land value is more affected by the growth in global wealth than any other locations in the world.

The situation is complicated/obscured by the fact that every economist and talking head on the television talks about house prices which shows a fundamental lack of understanding of what drives prices which is in fact land values.

As an aside, many of our members have stunning art, car and wine collections. Do they yield anything?? Are they going up in value? They don’t even have any utility.

But let’s look at the yield argument in a little more detail. Let’s say that you had £1m to invest in 2004. You could have bought a nice 2 bed flat in Chelsea or 40 houses in Sunderland. The two bed flat would have yielded c. 6% back then and the 40 houses would have yielded 10%.

Which do you think has made more money?

Indeed, earlier in the year, we bought an investment property in Knightsbridge for a gentleman who has c. 30 houses in the North-West of England. He has owned them for 10 years and although the yield is good, he is rather annoyed that there has not been any capital growth.

For the record, I used to own two houses in Sunderland which combined cost me a total of £50,000. The rebuild cost of each was £80,000 so the land actually had negative value.

Conversely, if you buy a £15m house in Belgravia, you will only insure it for c. £5m as that is the rebuild cost. In other words, it is the land that is the store of value and not the house. This is what conventional wisdom fails to grasp.

But what gives the land its value?

As towns grow the land became more valuable because the greater the concentration of talent and skills, the greater the opportunities. The best locations within the urbanisations command prime prices and as wealth expands and the infrastructure improves, so does the cost of the land.

This is obviously a highly simplistic overview, but the key point is that it is the land that increases in value and the landowner doesn’t have to do a thing because others – governments, companies and individuals – are paying to improve the infrastructure.

This is why it is unwise to rent over the long term because the tenant does not only pay for the roof over his/her head but also the ease of access to the local infrastructure.

The vital distinction is that the tenant pays for the infrastructure twice because he/she must pay taxes as well as rent, whereas the owner of the property buys the property and then has the tenants pay the mortgage while the owner benefits from the infrastructure improvements and subsequent increase in land value.

The landlord may temporarily have to pay towards the mortgage and there will be times when the land value falls temporarily, but this is insignificant compared to the increase in land value over time.

The most obvious example of this is The Duke of Westminster. Has he got poorer by holding onto property for the last few hundred years despite several crashes?

No, the 300 acres the family owns in Belgravia and Mayfair has exploded in value, but how much of that value has the family added? Obviously, they have made some investment themselves, but their wealth has been subsidised and boosted by all the other businesses and infrastructure that have made London great.

On a smaller level, just look at my parents’ generation who started buying houses – especially in London and the south-east – in the mid-1960’s. They have lived through three massive house price crashes but are sitting on huge gains (assuming they stayed in the market).

People who say London property is too expensive are simply wrong. This is not a politically correct point to make as large parts of it are too expensive for the majority of British buyers.

However, in terms of global wealth, there is no shortage of money available to buy – indeed, billions of pounds are just sitting on the side lines waiting and watching. This fact may be unpalatable for many Brits, but it is a fact (please note I am not making any moral judgements here, just highlighting how the market works).

But while some British buyers become priced out of the best locations by international wealth, the city evolves: Hackney, Shoreditch, Brixton and Shepherd’s Bush are now fashionable – and if you had said that would be possible in the 1980’s you would have been laughed at and quite possibly referred to a psychiatrist. Remember taxis did not go south of the river until 1996.

Does this mean property is a one-way bet? If a long-term hold then yes unless something cataclysmic happens (e.g. an industry is obliterated – think Stoke and pottery). However, there are better times to buy than others and there are certain properties that will outperform.

What is indisputable is that if you buy and hold good property in the most globally attractive locations you will reap the rewards by doing nothing but holding the land, because just as money isn’t distributed evenly amongst individuals, nor is it evenly distributed geographically.

Two points to note – firstly, by attractive I don’t mean the most scenic, but locations where people wish to congregate for business, pleasure, political stability, education, etc.

Secondly, I am not suggesting that you cannot make more money by setting up your own business, becoming a highly successful financier, etc. If you look at the Forbes Rich list or Sunday Times Rich list this is self-evident (it is also stunning how many billionaires are self-made which rather confounds many socialist arguments – that is a rant for another day!).

But what is also clear, is that if you study how these people invest their wealth, most of them have significant property portfolios as not only is it an exceptional store of value, but also a way to increase wealth, when bought well.

If you are looking for a legacy investment, there are few better options. And frankly, if you have the funds why not spoil yourself and own stunning properties around the world?

This is the prevailing attitude across the globe of those creating and inheriting astounding wealth. You just need to work out where they will want to spend their time and where is safe for them to invest.

As a little insight, in the last two months we have received membership enquiries from people looking for properties between £1m and £40m from the following countries: UK, Singapore, Spain, Italy, U.S., Hong Kong, Ghana, Nigeria, South Africa, Greece, Germany, Russia, Turkey and France.

It’s very easy for people to overlook the power of owning property. Despite the fact that landowners since the beginning of time have got wealthier and wealthier, people are easily distracted by the promise of getting rich quickly – crypto currencies, dot-com stocks (those with no business plans just .com after their names think 1999), penny shares, tulips, etc.

However, the safest way to remain wealthy is to simply sit on high quality land and property.

BUT…, you need to ensure the location remains high quality. There are areas in the north of England that were once very rich but are now destitute because the dominant industry has been decimated – steel, pottery, cotton mills, etc.

The same is true in the U.S. and, unfortunately, many small towns in Italy, Spain, Greece, etc. are dying as the young are fleeing in search of jobs and better prospects. And where do they head? To the affluent cities where opportunity beckons.

Could people flee London?

Of course, it’s possible, but it is unlikely to happen, because it has such a complex web of high-quality offerings which is hard to replicate – from finance to tech to biotech to education to culture to shopping to legal expertise to advertising to nightlife. I could go on, but I’m getting writer’s cramp.

In a report by Coutts, Hakan Enver, Managing Director at professional service recruitment company Morgan McKinley, puts it succinctly:

“What comes with this multitude of sectors are the huge volumes of job opportunities,” he says. “When compared to the difficulties in employment and vacancy numbers in other European countries, such as Italy, Greece and Spain, it is evident why London is a preferred destination.”

Even directors of the Bundesbank have said on Reuters that “London will remain the pre-eminent financial centre”, while Paco Ybarra, Global Head of Markets and Securities Services & Deputy Head of the Institutional Clients Group at Citigroup has said:

“I don’t feel this is the beginning of something gigantic and that London is going to lose its position as a global centre,” he said of Brexit. “But it’s a headache because we are all forced to reconsider how we do our business with clients in the EU.” He added: “I don’t have the feeling this is doomsday for London or the UK. It’s hard to see why it would be that significant. When we look at how many people we have to move, it’s not a big number.”

The fundamental point is that there is a huge amount of wealth sitting on the side lines due to all the uncertainty, much of which has been exacerbated by the focus on low probability worst case scenarios. But when this money is deployed land prices in the best locations have to increase.

Then add in more bank lending as regulations are relaxed (as they always are) and you can see how prices will actually fly higher in the global mega hubs and other destinations where the global elite wish to congregate.

Savills has calculated that there is £5.3 trillion in housing equity in the UK compared to just £1.4 trillion of mortgage debt. What do you think will happen when lending regulations are relaxed and people start to borrow more?

Prices will explode. This in turn will lead to massive speculation as people see property prices move higher while effectively having to do no work to generate the increase in value.

More people will jump on the bandwagon and this will lead to a final “crack up” boom which we see at the end of every cycle. Then there will be a monumental crash which will begin c. 2026 – put that in your diary.

But prices will be much, much higher than they are today and the increases will dwarf any losses in the crash if you buy early enough. For example, if you bought well in London in 2005 your property was still worth more in the depths of the crash than what you paid.

Meanwhile high yielding properties in areas like Sunderland and Newcastle have only just got back to their 2007 levels. Do you still want to focus on yield now???

Consequently, some of the most successful families and entrepreneurs are taking advantage of the uncertainty caused by Brexit: Li Ka Shing is actively acquiring property in London while the FirethornTrust which is run by two of America’s wealthiest families are also active:

“Brexit in its current status causes uncertainty,” Peter Mather, one of the FirethornTrust’s founding partners told Bloomberg. “The uncertainty causes volatility, and the volatility causes opportunity.”

We have recently bought several properties for our members and are seeing a marked increase in the number of active buyers. Yes, the numbers are still low compared to normal levels but that is the great irony of a buyers’ market – the masses don’t buy and then pile in when it is too late.

Astute buyers are actively looking now, but you must be selective. There are plenty of exceptionally poor and average properties in Knightsbridge, Belgravia, Mayfair, etc., which will underperform the market, so please don’t think that just because you are buying in prime central London that you are guaranteed success.

I have personally inspected over 23,000 properties for our members and seen the details of c. 50,000 more but we have bought under 1% of these. That is how selective you need to be.

As I point out in my book on how to succeed in the London property market, you must buy best in breed:

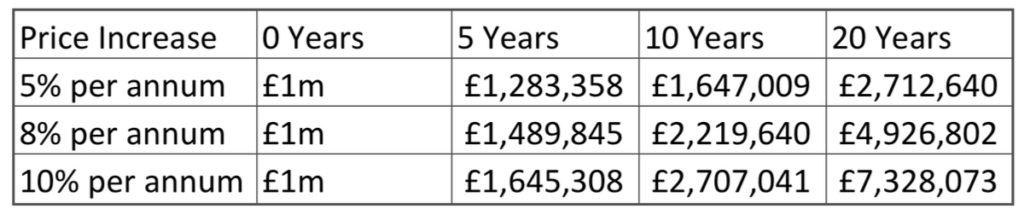

Research by Savills has shown that between 2005 and 2013 the top decile of prime London property increased by 190% while the bottom decile only increased by 63%.

This outperformance can be seen in the chart below: If you bought a property for £1m this is what would happen:

As you can see, over the long term the difference of just a couple of percentage points’ outperformance can be huge.

I know I bang on about this, but it can’t be overstated even if your focus is on buying a home rather than an investment. Of course, you want a stunning property that will be a safe and fun home for your family, but this doesn’t mean you have to forego the performance.

I am not suggesting that you rush headlong into the market. You must find the right opportunity. However, you should start as soon as you have the funds ready and that doesn’t mean start looking at the websites – as my book, The Insider’s Guide To Acquiring Luxury Property in London, reveals, you will not find the best opportunities that way.

You need to be actively looking, because even if you don’t find a suitable opportunity immediately, you need to have a better understanding of the market, so that you are ahead of other buyers when they jump back into the market. Because what do you think will happen when there is greater certainty?

It’s called a window of opportunity for a reason. The opportunities do not hang around. You only find them by being constantly active. Hoping that you can find a great home or investment opportunity just by calling an estate agent occasionally or looking at websites like the thousands of other buyers is wishful thinking.

And the reasons why people need to sell vary dramatically, so don’t obsess about what the market in general is doing. You only need to find that one property that will be your ideal home or investment and is a situation where the seller is keen to transact so that you can acquire it at an attractive price.

So, do start actively looking while remaining selective.

Of course, before you start you may like to know more about:

- How to accurately value properties so that you don’t make an expensive mistake

- The most effective ways to negotiate with the estate agents

- How you can find the best opportunities with the minimum of effort

- What exactly is happening to the market in your target areas and price range

Or you may have other questions or issues, e.g. you are simply too busy to undertake the task of buying a home by yourself.

So, if you or your clients would like to discuss any of this in more detail, simply call my assistant, Veronika, on +442034578855 or email [email protected] to schedule a meeting with me.

Best regards,

Jeremy McGivern